The Fed has raised rates 5 times this year (March, May, June, July and September).

While this impacts many things, the cost of housing is significantly affected, as shown in the visual comparison below:

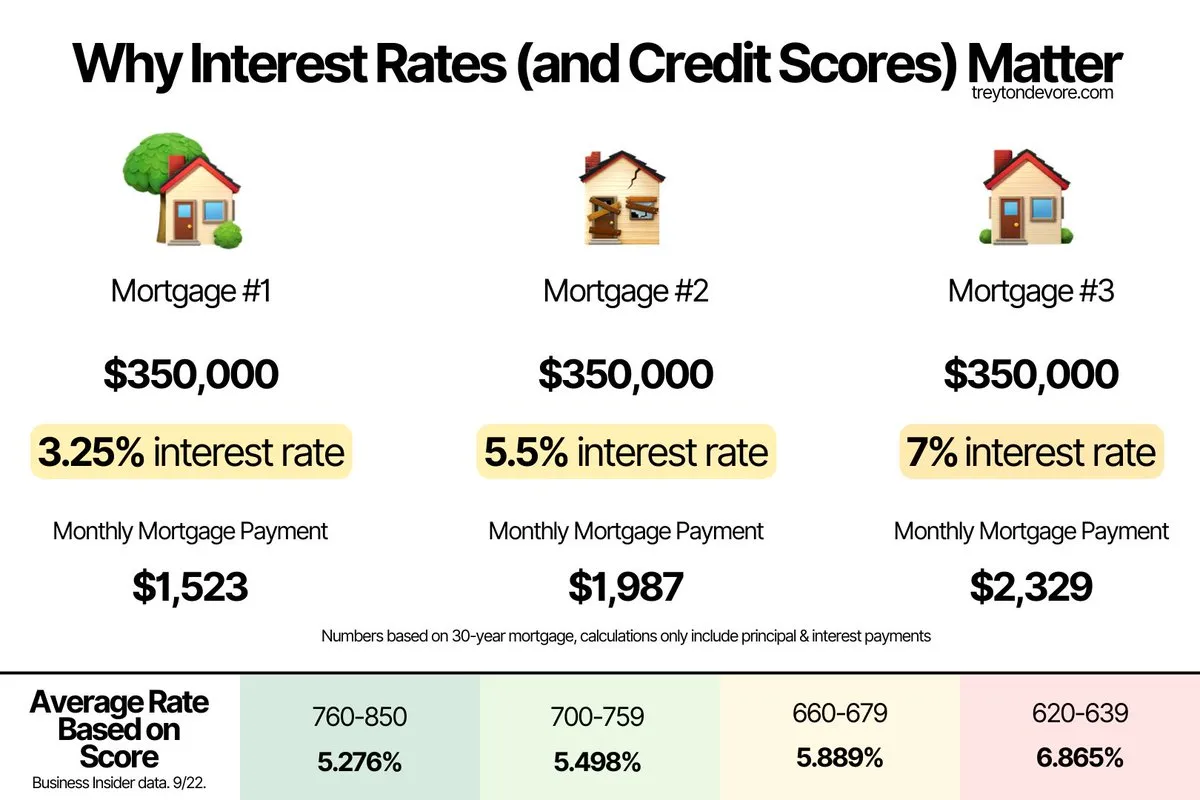

Simply put, a 3.75% increase on a mortgage could cost you an extra $9,600/year or almost $300,000 over the length of the loan (on the same house) 🤯

It's expected that the Fed will raise rates at least a couple more times before the end of the year, so I wouldn't be surprised if we see mortgage rates reach 10%+ beginning early next year.

If you bought a home during the pandemic, congrats - you won the home ownership game. If you were planning to buy in 2023 like I was, we just missed the low-interest rate boat..

But one way to fight off higher rates is to maintain a high credit score (shown in the graphic).

Even though the rate will still be higher than previous years, a higher score will help you qualify for the best rates available.

Another option is to put down a larger down payment so that you get a slightly lower rate and you're paying less on the mortgage.

Either way, all consumer debt (credit cards, car loans, mortgages, etc.) will continue to increase in cost and the only way to avoid it is to keep your debt to a minimum.

If you have loans with variable rates, it might make sense to pay more towards them now so you don't incur higher costs when they adjust.